“What’s the average return I should expect from my investments?” It’s a common question we hear from clients when discussing new investment options, portfolio performance, or in general discussion.

While it’s clear the intention of the question is meant to understand the opportunity for growth, should the question be phrased a little differently to get a more accurate response?

We believe the answer is ‘Yes’.

In the original question, “What’s the average return I should expect from my investments?” there is one key word that must be changed, average. Why the change? The reason is that average returns do not properly factor the detriment of negative returns.

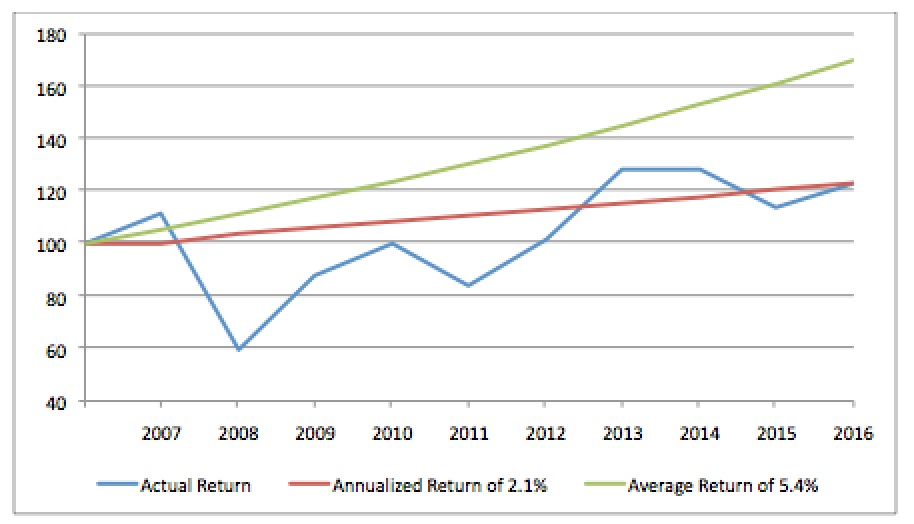

Finding an average is one of the things most of us remember from elementary school math, but let’s do a quick example to make sure we’re all on the same page. To find the average you simply add up all the numbers and divide by how many numbers there are. In this example, we’re looking at the annual returns from the Dodge and Cox International Stock Mutual Fund (Ticker: DODFX). The average net return for the last 10 years is as follows (source Yahoo! Finance. Performance through 12/31/2016):

11.7%+,46.7%.+47.5%+13.7%+,16.0%.+21.0%+26.3%+0.0%+,11.4%.+8.3%-10.=5.4%

5.4%! While the international stock market has been volatile over the last decade, most investors would be satisfied with 5.4%. 5.4%, however, is not truly your return. As discussed above, average returns do not properly take into account the loss of capital associated with negative returns. Back to our example of the Dodge and Cox mutual fund above:

Let’s say you have $100 and invest your money in the mutual fund at the beginning of 2008. One year later you now have $53.30 due to the 46.7% loss. That 46.7% loss of capital will now take you a positive 87.6% return just to get back to your original $100! This unfortunate negative return is not properly accounted for in a simple average.

A Solution

Back to our original question: “What’s the average return I should expect on my investments?” To receive an accurate response your question should be phrased “What’s the annualized return I should expect?” This new term ‘annualized’ will fully represent the detriment of negative performance on your investment dollars. Finding the annualized return using the example above takes a few additional steps that are slightly outside the scope of this post but what we are technically doing is finding the geometric mean of the annual returns. The answer we find using this method is actually quite surprising. The annualized return for the fund is only 2.1%, a full 3.3% lower than the average return! Not nearly as satisfactory as the 5.4% you expected when asking for average return.

Any time you are reviewing performance of your portfolio, (a mutual fund, ETF, annuity, or any other investment option) you should be sure the performance your viewing is an annualized return, not an average return. This mathematical solution takes into account the negative consequences of down years to provide a more accurate return over a given time period.

Always knowing to ask for annualized returns on your investments will put you one step ahead when sifting through the many types of investments presented to you.

As always, please feel free to reach out to your specific advisor with any questions or comments.