In the right hands, credit cards can be a powerful financial tool. They add protection and convenience to the transactions we make every day. Oh yeah, they also have reward points. Not sure if you knew that… We all love points, but it can be far too easy to get caught up in the allure of points and miles. While they can be a great reward for someone that uses their credit card wisely, you could be on the losing end of compounding interest if you’re not careful. Like Spiderman’s Uncle Ben says, “With great power comes great responsibility”. Read on to learn about the true cost of credit cards to make sure you’re not getting caught up in the points trap.

Minimum payments and cumulative interest

“But I’m paying what I’m supposed to!” is a phrase I’ve heard a couple hundred times from clients working to dig themselves out of mountains of credit card debt. What they are typically referring to is the card’s minimum monthly payment. The minimum payment on your card is calculated as a percent of your current balance. Normally, this percentage is around 2% of the balance on the card. To make sense of all this credit card talk we’re going to get into, we need to take a second to create an example credit balance and APR or Annual Percentage Rate.

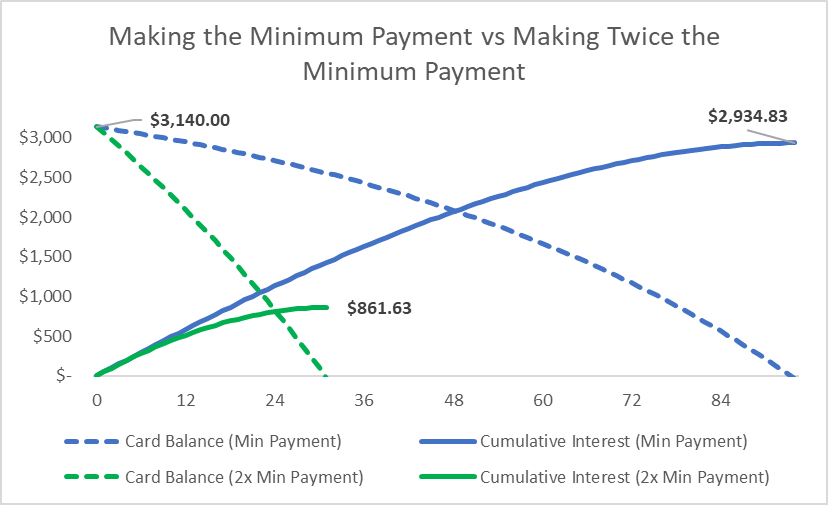

According to information from the Fed (https://www.newyorkfed.org/microeconomics/databank.html), the per capita credit card debt balance for people living is Pennsylvania is $3,140. To put that in perspective, that’s all of the credit card debt in PA divided by every person with a credit report. That’s a lot of debt to go around! From personal experience, of the people I’ve worked with that carry credit card balances, the balances are, unfortunately, around three times that amount. So, while people saddled with credit card debt might be facing down a larger balance, I think credit card debt per capita will work well as an example. As for APR, according to the credit card info aggregator, www.wallethub.com, the average APR for new offers is 19.21%. Sure, that’s well over Pennsylvania State usury laws but lucky for the card companies, they can be based in any state they want and surprise, surprise, they choose to base themselves in states that allow them to charge almost however much they want!

Back to the minimum payment. So, the minimum payment on a card with a $3,140 balance will be around $65 per month. In real life, as the balance on the card decreases, the minimum payment will decrease to a point as well. The credit card companies are, of course, ok with this because it stretches out the time that you are paying their favorite thing, interest! In this example, though, we are assuming that you begin by paying the minimum payment on the balance and continue to pay that amount until the debt is paid off. By only paying what you are “supposed” to, with a 19.21% interest rate, it would take just shy of 8 years and $2,934.83 in interest to pay down the original $3,140 balance! This is assuming that you stopped using the card and are not adding to the balance along the way. It’s very important to look at that minimum payment not as what you are “supposed” to pay but for what it is, the bare minimum you can pay in a month to avoid a negative credit report.

Because no Innova blog post is complete without a graph, let’s take a visual look at how much better the situation gets when we pay more than the minimum on the same balance and interest rate. In this case, we’ll double the minimum payment of $65 to $130 a month.

As you can see, by doubling the payment, the debt was paid down five years and four months earlier and the total amount of interest paid was cut down by around 70%!

0% APR Offers

I know what some of you are thinking. “Sure, those suckers that pay such high APRs have to worry about all of that cumulative interest, but not me, I’ll transfer my balance to a new card with a 0% APR offer!” I know of plenty of people that do the balance transfer jump from one 0% APR offer to the next. A move like this can be useful in paying down a high interest credit card debt but it carries its own risks. For one, there are typically balance transfer fees of 3-5%. A $5,000 balance transfer will cost you $250 to move to another card. If the plan is to pay down the debt, this fee may be well worth it. However, I have seen far too many people treat a balance transfer as a stepping stone until the next offer comes their way. They will pay the balance transfer fee with each jump along the way with no intention of paying down the balance. This might work for a while but at some point, the music will stop and a large balance will need to be paid with interest.

0% APR offers can be really exciting even for people that are not looking to transfer a balance. Big box stores are constantly dangling a 0% APR for 24 months deal on large purchases in front of us and for many, it’s a great option. A deal like that can make a large purchase much more palatable by allowing you to stretch out your payments without paying interest. Of course, this only works well if you are able and willing to keep up with the payments and pay off the account by the end of the 0% APR period. If you don’t, you may be forced to pay a much higher interest rate on the remaining balance. Some cards even force you to pay interest starting from the original balance of the purchase.

Points

Points and miles are a great incentive to use credit card in a responsible way. There are loads of different reward structures for whatever your interests may be. Miles, cash back, discounts on purchases from certain places are all available to you. It’s important to view them as reward for smart use of your credit instead of as an excuse to continue using a card you are carrying a large balance on. Let’s say that card from our first example was an Amazon credit card that offers 5% back on purchases from Amazon. Spending $3,140 on your Amazon card, all at Amazon, will net you $157 in rewards points. Sure, you can do some damage in the Deal of the Day section with that kind of scratch but that $157 in rewards is a drop in the bucket compared to the $3,643.46 you’ll pay in interest over time by paying only the minimum payment.

Points are a great way to treat yourself when you’ve been diligently handling your finances because they are only beneficial to you when you do not carry a balance from month to month.

What to do about too much credit card debt.

When we find ourselves in the grips of too much debt, it’s useful to take one step at a time. High interest credit card debt is typically the first type of debt that should be paid down. It’s easy to see from the previous example how even $3,140 in credit card debt can cost you several thousands in interest. The first step is nearly always to cut up your credit cards. Debt pay down strategies are impossible to complete when debt is continually piled on top. A home equity line of credit may be a short-term fix as this will shift high interest revolving debt into a more manageable payment with much lower interest. It’s very important here to understand that using a home equity line of credit to pay down your cards is not to allow you to keep spending. You’re essentially using it to put out a “debt fire”. Once the fire is under control, you have to examine the habits that got you there in the first place. These habits need to change!

Credit cards offer a lot of great benefits when used responsibly. If you have questions on how to manage your credit card debt or even if you want help to find the best credit card that will work for you, give us a call at 888.270.1574

Innova Wealth Partners, LLC (“Innova”) is a registered investment advisor. Information presented herein is for educational purposes only and does not intend to make an offer or solicitation for the sale or purchase of any specific securities, investments, or investment strategies. Investments involve risk and unless otherwise stated, are not guaranteed.

Readers of the information contained on these performance reports, should be aware that any action taken by the viewer/reader based on this information is taken at their own risk. This information does not address individual situations and should not be construed or viewed as any typed of individual or group recommendation. Be sure to first consult with a qualified financial adviser, tax professional, and/or legal counsel before implementing any securities, investments, or investment strategies discussed.

Any tax information and estate planning information contained herein is general in nature, is provided for informational purposes only, and should not be construed as legal or tax advice. Innova does not provide legal or tax advice. Innova cannot guarantee that such information is accurate, complete, or timely. Laws of a particular state or laws that may be applicable to a particular situation may have an impact on the applicability, accuracy, or completeness of such information. Federal and state laws and regulations are complex and are subject to change. Changes in such laws and regulations may have a material impact on pre- and/or after-tax investment results. Innova makes no warranties with regard to such information or results obtained by its use. Innova disclaims any liability arising out of your use of, or any tax position taken in reliance on, such information. Always consult an attorney or tax professional regarding your specific legal or tax situation.

Innova has been nominated for and has won several awards. Innova did not make any solicitation payments to any of the award sponsors in order to be nominated or to qualify for nomination of the award.