ETF v. MF

In our February newsletter, we’ll look at two major investment vehicles in the current investment landscape; mutual funds and exchange traded funds or, ETFs. We’ll run down the key attributes of a mutual fund and an ETF and two of the key differences between them; fees and taxation.

History

Mutual funds are almost universally known. Introduced to the US in the 1890s, mutual funds became widely used in the 1920s. From that point to today, mutual funds have been the dominant investment type in everything from 401(k) plans to individually held IRAs and even variable annuities.

Many people believe ETFs are a brand new investment product as they have recently generated a lot of attention. While relatively new, ETFs have been used by investors since 1993. In that time period, the amount of ETFs on the market has exploded. What has caused this large influx of investments in ETFs? We’ll dive into both mutual funds and ETFs to find out.

What is a mutual fund?

Mutual funds start with a pool of money collected from many different investors. A fund manager takes this pool of cash and invests it in individual stocks, bonds or commodities in attempt to accomplish a specific goal. For example, some mutual funds look to provide income from dividend payments; others try to perform better than a certain market segment. This pool of invested money is divided up into mutual fund shares that are held by whoever paid into the fund. These shares increase or decrease in price depending on the value of the assets purchased by the fund manager and the share value is calculated at the end of each day. As more investors add money, more assets are purchased and more shares are created. When an investor wants to sell their shares, they sell them back to the mutual fund company and the mutual fund manager sells holdings to return the investor’s cash.

What is an ETF?

Exchange traded funds are similar to a mutual fund in that they are an investment product that contain many underlying individual stocks, bonds or commodities. ETFs differ from mutual funds in many ways, however. Two key ways in which they differ are 1) ETFs are traded between investors throughout the day and 2) most ETFs only attempt to mimic a market segment, not outperform.

In both cases, mutual funds and ETFs offer an easy way for investors to diversify their investments amongst many individual holdings. So if mutual funds are used by everyone and anyone, why bother learning about ETFs? If it ain’t broke, don’t fix it, right? Well that second point has been scrutinized a lot more lately. Turns out, mutual funds have more than a few issues. The two we’ll focus on today are 1) internal fees and 2) the lack of control over taxation. Let’s take a look at some examples.

Fees

While fees within mutual funds have been slowly reducing (largely due to competition with ETFs), the internal fees are still very high. According to Morningstar’s 2015 Fee Study, the equal weighted average mutual fund fee was found to be 1.19%. This creates a large hurdle for returns to overcome and can cause a meaningful drag on performance.

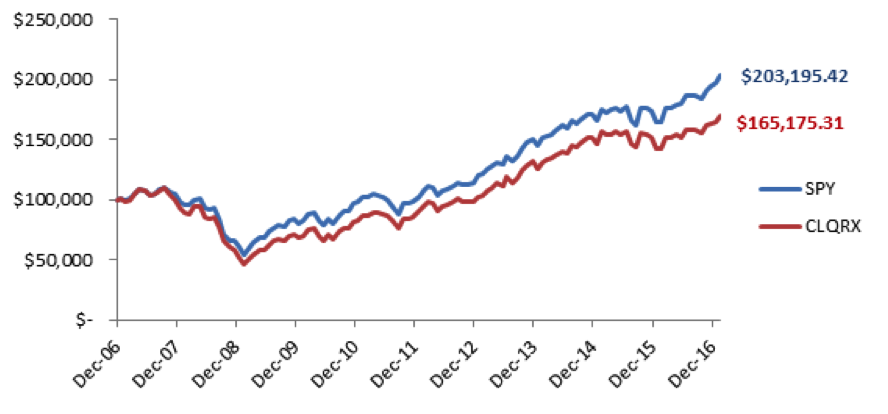

Let’s take a look at the Columbia Disciplined Core (CLQRX), a Morningstar Medalist fund. CLQRX has an R-Squared of 96.15% with the S&P 500. I know, I know, fancy math talk. It’s actually really easy to understand. An R-Squared of 100% means all of the fluctuations in a fund can be explained by fluctuations in the index it’s compared too. So in plain English, the Columbia Disciplined Core fund moves almost exactly in line with the S&P 500 Index. That’s all well and good but holders of the Columbia Disciplined Core Mutual Fund are paying a 1.29% fee for the privilege of basically matching the index. Below is a chart of monthly returns since the fund began in 2006 compared to an S&P 500 index ETF, the SPDR S&P 500 fund (SPY). SPY has an internal fee of 0.09%, over a percent less than the Columbia fund. Because of this, SPY has a much smaller fee hurdle to overcome than CLQRX. The chart below details what a $100,000 investment in each fund back in 2006 would look like over the ten years following. All price data was sourced from Yahoo Finance.

The strong correlation between the Columbia fund and the market index is pretty easy to see by looking at the lock step the two funds move with each other. A little tougher to notice is how a large part of the around $38,000 difference in final values is due to the over 1% difference in internal fees. This huge disparity only gets bigger over time. If the Columbia fund acts so much like the S&P 500 ETF, why pay so much extra in fees?

Taxation

As we learned, a mutual fund share is a piece of the pool of investments managed by a fund manager. The fund manager is constantly buying and selling within the fund for a variety of different reasons. Sometimes to rebalance the fund, other times to generate cash for investors that would like to redeem their shares. This constant trading activity is not tax free. So who pays for the capital gains generated by the trading within the mutual fund? That’s right, the shareholder. Each shareholder is responsible for part of the capital gains that occurred within the mutual fund. This capital gains liability can come as a complete surprise for many investors. ETF investors deal with a capital gain or loss when they sell their shares and not at the whim of a fund manager.

We’ve only scratched the surface in our exploration into Mutual Funds vs ETFs. Both mutual funds and ETFs offer ease of diversification. However, high investment fees and low control over taxation associated with mutual funds have given ETFs an edge. In a world where returns are becoming increasingly hard to come by, any drag on performance from excessive fees or tax inefficiencies needs to be examined. Contact us today if you’d like to know more about how ETFs can fit in your investment portfolios.

By: Jon Inzero, CFP®