Is Too Much Information Bad for Investors

It’s hard to imagine a world where investors had to wait until the next day’s Wall Street Journal to find out how their holdings did the previous day but that actually wasn’t long ago. Now with a swipe of a finger on an iPhone you can get stock prices, research reports, analyst ratings, recent earnings etc. We can track the value of our portfolios on a second by second basis, when you think about it it’s kind of incredible. It begs the question however, is this good or a bad for investors?

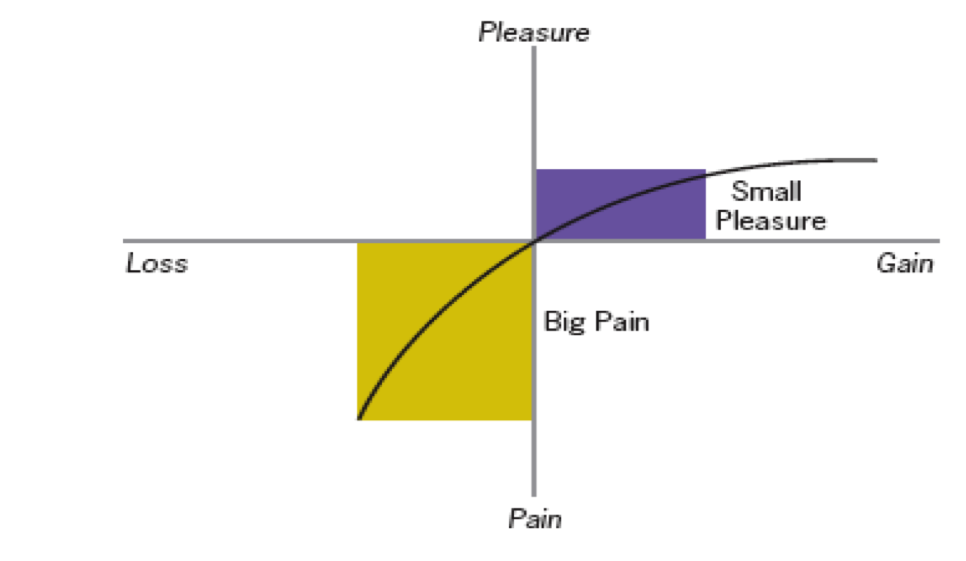

If everyone was totally rational (we know from experience this isn’t true) then it wouldn’t matter how often people valued their portfolio. They’d accept the moves knowing that (hopefully) it was part of a long term plan to get them to where they ultimately want to be. That sounds all well and good until you actually experience those moves. In his book Nudge (which we highly recommend) Richard Thaler talks about a concept he calls “myopic loss aversion” which states that people hate losses more than they like gains and that those same people tend to evaluate outcomes very frequently. Through experimentation (and in his book “Thinking Fast and Slow” – which we also highly recommend) Nobel Prize winner Daniel Kahneman puts a value on people’s feelings of loss vs gain at 2:1. What he found was that people felt that it was better not to lose $1 than it was to find $1 and the value of that feeling was 2:1 in favor of not losing money.

Here’s what that might look like in a text book……

And here is a simpler way to show it…..

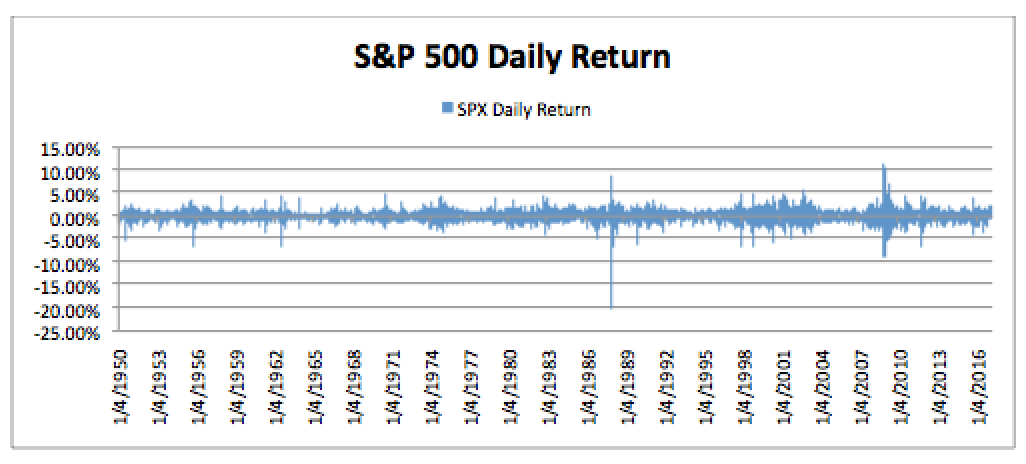

How does this relate to my portfolio you might ask? Let’s take a look at some data first. Below is a chart of the daily returns of the S&P 500 from 1/4/1950 to 2/28/2017 (all data from Yahoo Finance, calculations by Innova Wealth Partners WEALTH PARTNERS). I know it’s almost impossible to make any sense of it so let’s summarize below.

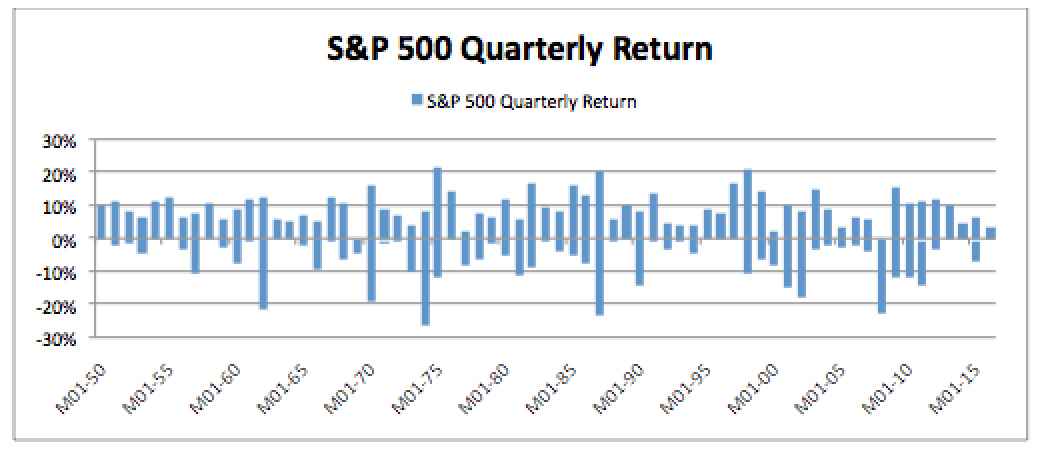

The average daily return of the S&P 500 was +0.03%, barely positive! The market produced a negative return on 46.4% of days and a positive return of 53.6% of the time. This was basically a coin flip! What happens when we take a step back and look at quarterly returns? The chart below should shed some light.

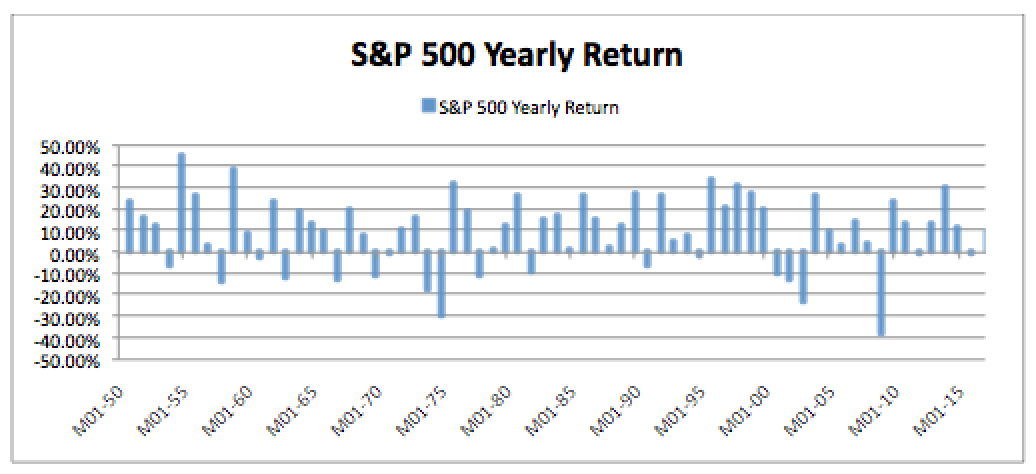

Hopefully the picture becomes slightly clearer, here we have an average quarterly return of +2.14% and only 34.3% of quarters are negative while 65.7% of quarters are positive. See where this is heading yet? Let’s take one last look and target annual returns.

Below is the chart and I‘ll also summarize the results.

This should be the most clear of the charts, when examining annual returns we find the average is a substantial 8.94% and 73.1% of them are positive while only 26.9% of annual returns are negative. So why did we spend so much time digging through that data and explaining it to you?

If the stock market is basically a coin flip between positive and negative returns on any given day and we check our portfolio every day (sometimes many times per day – YOU KNOW WHO YOU ARE) you’re essentially guaranteed to see more losing days! If people hate losses more than they like gains at a factor of 2:1 then we’re locking in the fact that we’ll feel awful about seeing short term losses in our accounts even though they’re totally normal in a long term strategy! The less frequently you take a peek at your portfolio the more likely you are to see gains because the odds that your portfolio value has risen increase as holding your period increases. It’s a great way to try to avoid making an irrational decision based on emotion and not facts and data.

Now we’re not crazy enough to believe that after reading one post you’ll only look at your portfolios every quarter or year (nor do we recommend this) BUT now at least when you do check more frequently you’ll be armed with the knowledge that you’re making yourself susceptible to “myopic loss aversion” and can hopefully avoid making any rash decisions.

Not checking your portfolio that often and STILL not feeling great about how everything’s going?

Here are some great additional resources:

By: Ian Foster