What do the words racecar, level, deified and kayak all have in common? They’re palindromes, which means they’re the same word if you reverse the letters. Pretty cool, right? Today we’re going to look at whether Retirement is a palindrome, but first let’s set the stage.

Has everyone seen the movie Back to the Future II? It’s the one where Biff was rich because a future version of himself came back in time and gives him a sports almanac from the future. Knowing all the winners in advance is a sure thing and Biff becomes famously wealthy betting all the games.

Now, imagine that it’s October of 1999 and a future version of yourself appears on the day you are about to retire and hands you a newspaper with all the closing prices of the major markets 20 years into the future. That would be a good day indeed! You quickly do the math and find out that the best performing market over the next 20 years annualized 5.5% returns, “ok, I can work with that” you think as you start to get excited. With this information you quickly decide to invest your entire nest egg into that market. Let’s assume you’ll enter retirement with a $2,000,000 portfolio, imagine what that will grow to in 20 years with 5.5% returns. If you’re like us (probably not – we’re finance geeks) a picture like this would start to form in your heads:

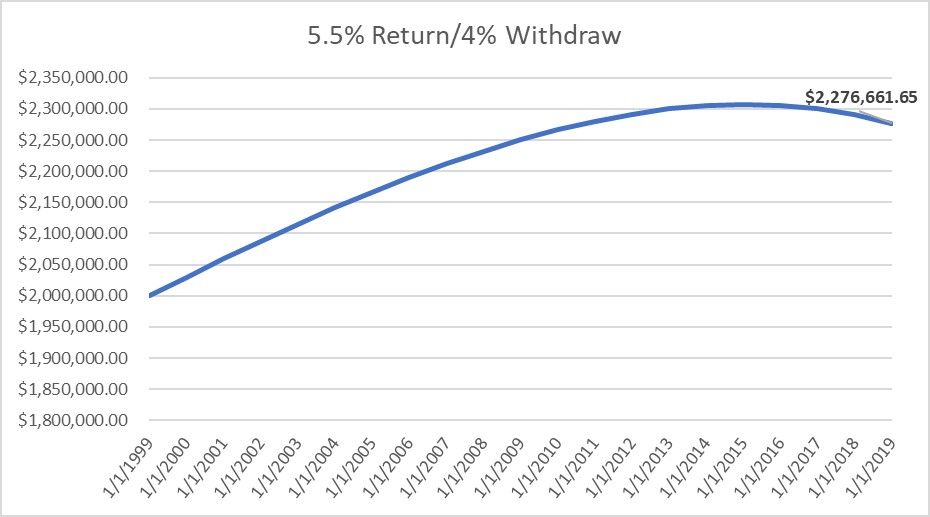

It turns out that over 20 years your $2,000,000 portfolio would grow to a whopping $5.8 million! Well, not so fast, you are about to entire retirement so you’ll need to use this portfolio to fund your lifestyle. You’ve heard people mention that the “rule of thumb” is a 4% withdrawal from your portfolio each year (adjusted for inflation) will almost guarantee that you don’t run out of money. So, next you run some more calculations in excel and come up with this chart, this is a $2,000,000 portfolio growing at 5.5% taking $80,000 (4%) out to live (again – adjusted for inflation @ 3%/year):

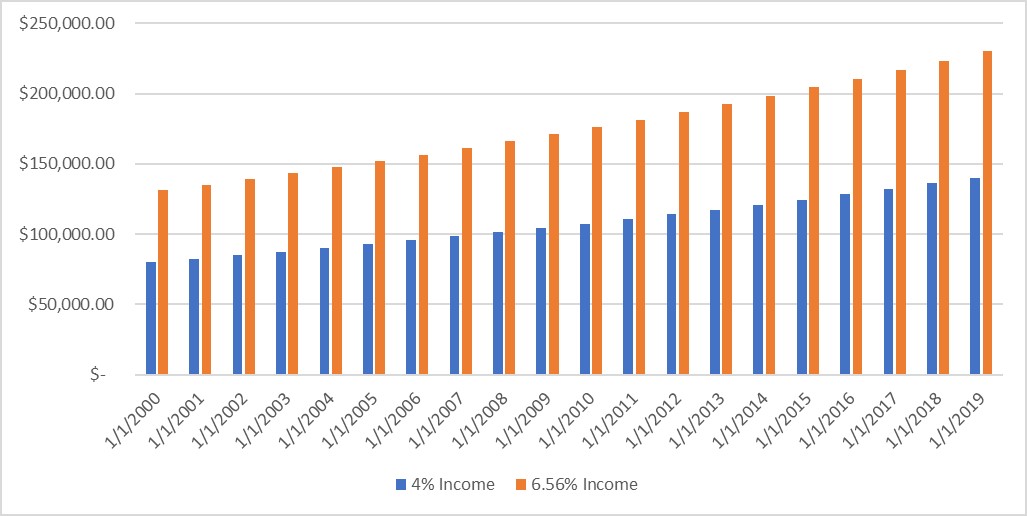

Ok, this isn’t as great as ending with $5.8 million but still not too shabby! You actually wind up with more money than you started with after 20 years while fully funding your retirement. Not bad at all! That last point sticks with you and you start to think, that “4% rule of thumb” is for the other people who don’t know what you know. You know what the best performing asset class will be so while those people have to deal with uncertainty you don’t! What do you do next? Well if you know what your returns are going to be, and you’re relatively clever with excel, you figure out how much you can withdraw each year (again adjusted for inflation) so that you spend as much as you can in retirement while not running out of money. Your eyes light up when you see the result. You can withdraw 6.56%/year (once more – adjusted for inflation) and you’ll have your last check bounce at the end of 20 years. What does that look like as far as your spending? Below we show the income of a 4% withdraw vs a 6.56%:

That is a serious increase in your spending in retirement! You are really feeling pretty good about how everything’s turning out now! Next thing you know you’re looking at vacation homes and that sweet red sports car you didn’t think you could afford until this morning!

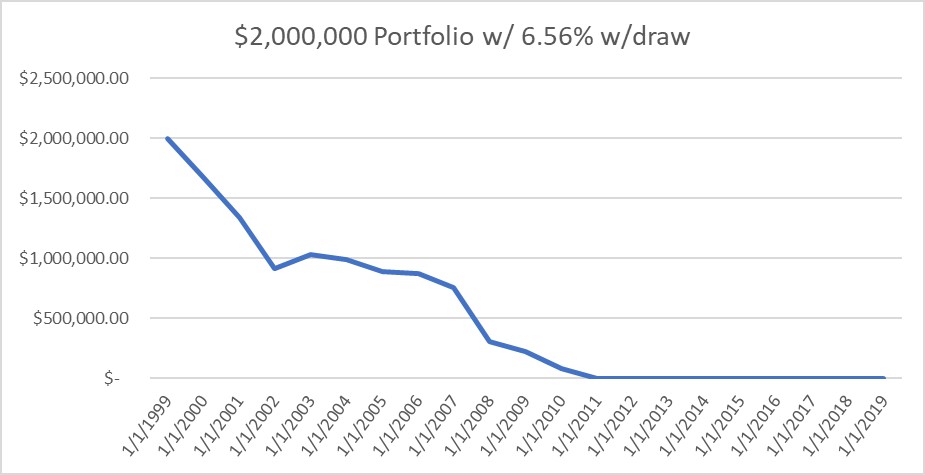

So far, we’ve been looking into the future using the information your future-self gave to you. It’s time to take a look at how things actually would’ve turned out using that information to plan your retirement. It turns out that the best performing market was the S&P 500 and it did indeed return an average of 5.5% over the next 20 years. Here’s what a $2,000,000 portfolio invested into SPY (S&P 500 ETF) would’ve turned into over 20 years:

If you remember the first chart, you’ll recognize that ending dollar amount. So far so good! Now we’ve just got to adjust the chart to account for the withdrawals we’re going to make in retirement (6.56%/year adjusted for inflation) since we know the future! Aaaaaaaaannnnnnndddddd here it is:

Uh oh! What happened?!?! Here, in the real world, you ran out of money in just over 10 years! You had run all the numbers, triple checked your work, and thought you had a huge leg up on the rest of the world, what went wrong?!?!?!

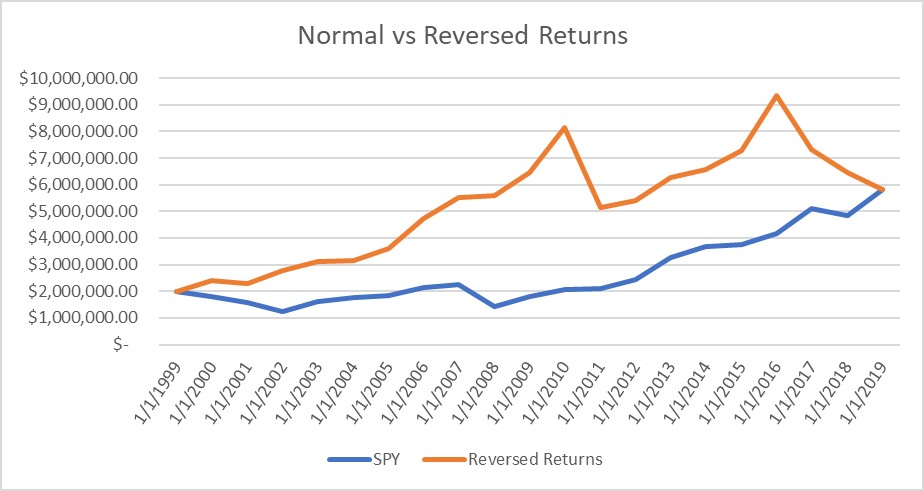

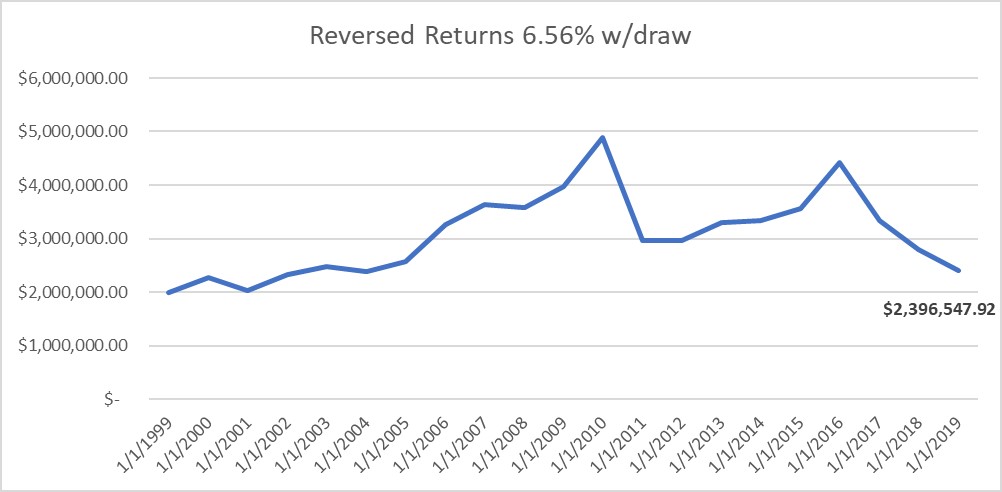

It turns out that in retirement (or any other time you’re taking withdrawals from a portfolio) the journey means just as much as the destination. What do we mean by that? The sequence, or order, of the returns you get each year make a huge difference in whether or not your successful. As an example, let’s reverse all the returns (like letters in a palindrome) so that 2019’s return comes first and we end with 1999’s return. Here’s a chart to show you end up in the same place if you’re just investing a lump sum:

So far so good, we end up in the same place. Now let’s take a look at the reversed returns with a 6.56% annual withdrawal adjusted for inflation:

Wow! What a difference that makes. Here, we have the same exact annualized returns simply reversed and we go from running out of money in just over 10 years to having more than we started with after 20!

So why does this matter? It matters because there will ALWAYS be a “best performing” asset that you’re most likely not invested 100% into, and that’s ok. It’s important, especially in retirement, that you hold a diversified portfolio that minimizes the amount of risk you take while maintaining your growth requirements. The highest returning assets almost always have the highest amount of risk, or volatility, as well. If that risk manifests itself at an unlucky time (early in your retirement) all the amazing returns in the future won’t help because you’ll be left with so little at that point they won’t matter. Would you want pure luck to determine the success of your retirement? Probably not!

Now, to answer the question in the title of this post: NO! Retirement is NOT a palindrome and I hope the info in this post showed you why. I guess we could’ve saved a bunch of time and just tried to spell it backwards too……..

Innova Wealth Partners, LLC (“Innova”) is a registered investment advisor. Information presented herein is for educational purposes only and does not intend to make an offer or solicitation for the sale or purchase of any specific securities, investments, or investment strategies. Investments involve risk and unless otherwise stated, are not guaranteed.

Readers of the information contained on these performance reports, should be aware that any action taken by the viewer/reader based on this information is taken at their own risk. This information does not address individual situations and should not be construed or viewed as any typed of individual or group recommendation. Be sure to first consult with a qualified financial adviser, tax professional, and/or legal counsel before implementing any securities, investments, or investment strategies discussed.

The tax information and estate planning information contained herein is general in nature, is provided for informational purposes only, and should not be construed as legal or tax advice. Innova does not provide legal or tax advice. Innova cannot guarantee that such information is accurate, complete, or timely. Laws of a particular state or laws that may be applicable to a particular situation may have an impact on the applicability, accuracy, or completeness of such information. Federal and state laws and regulations are complex and are subject to change. Changes in such laws and regulations may have a material impact on pre- and/or after-tax investment results. Innova makes no warranties with regard to such information or results obtained by its use. Innova disclaims any liability arising out of your use of, or any tax position taken in reliance on, such information. Always consult an attorney or tax professional regarding your specific legal or tax situation.

All data for the charts and graphs in this post was sourced from “finance.yahoo.com”. All calculations done by Innova Wealth Partners, LLC.