Part 2 of our letter will offer some tips and strategies to move you closer to that early retirement!

In your 20’s – Save Early and Save Often

In your 20’s, you have one of the most valuable investing tools to work with… Time! Investing over multiple decades allows the power of compounding to dramatically increase your nest egg. And since we’re talking about an early retirement, the earlier you start saving the better. Setting aggressive savings goals early in your career will help create positive habits. Aggressive savings can mean different things to different people, so let’s target a minimum savings rate of 30% of gross income.

This level of aggressive savings will have other positive effects for our young individual or couple. First, the IRS provides tremendous tax benefits for saving through an employer sponsored retirement plan. If the traditional (non-Roth) plan is chosen, this will provide a tax-deduction. If a Roth plan is chosen, then those saved dollars will grow tax free! Second, it is common for employers to entice employees to save by offering a match. This will help bolster your retirement savings and make early retirement even more attainable!

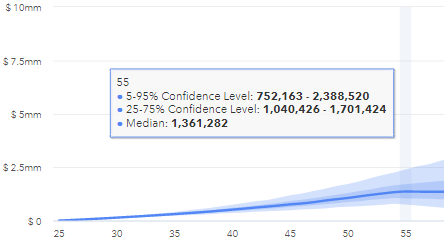

Let’s use a hypothetical couple that are both 25 years old as an example. Each individual makes $40,000 per year (3% annual raises) and has set their sights on retiring early at 55. They know they must save aggressively so both save 30% of their salary. Each of them puts their savings into their company sponsored retirement plan with a 60% stock/40% bond allocation and is eligible to receive a 2% company match as well. As a result (depending on market conditions while they’re investing) using a Monte Carlo simulation with 1,000 different trials, our couple would successfully retire at 55 with over $1,040,426, 75% of the time! That does not mean that the other 25% of situations are totally unsuccessful, but spending changes must occur during retirement to keep them on track.

In your 30s – Master Your Budget

Your 30’s can become a time when expenses cut dramatically into your ability to save. Many ‘events’ that require tremendous cash outlay dig into income & savings and easily derail your early retirement goals. These can be any or all of the following: buying a home, getting married, and having children. Successful budgeters realize all of these major life events don’t need to break the bank and derail the fantastic savings habits that you established in your 20s. It can be difficult for many couples and growing families, but staying above that 30% savings threshold and avoiding expensive debt (credit cards, personal loans, or payday advances) will keep you on track through your 30’s for that early retirement goal!

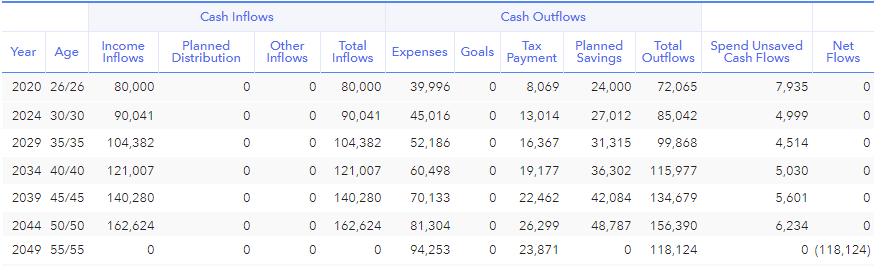

As we mentioned above, just because our couple did not hit the $1,000,000 mark in about 25% of simulations does not mean their retirement isn’t a success. Any couple that has the capability to save at this level is likely going to live within their means. Since our couple started saving 30% of their income in their 20’s, they also learned to live on $4,005/mo, including taxes at that time. Assuming inflation of 3%, that same lifestyle will cost them $9,843/mo when they retire at 55. While this would potentially be unsustainable in retirement as a sole source of income, our couple knows later in retirement that social security will help support their lifestyle. The chart below shows the savings and spending habits of our couple every 5 years through their working lives and into the first year of their retirement.

In your 40s – Target a Debt Free 50th Birthday!

Most successful retirements, including those looking towards an early retirement, are debt free. Reason being is most debt (mortgages, car payments, credit cards, student loans, lines of credit) must be repaid. This usually occurs in monthly installments, driving up your cost of living. Since supporting your everyday expenses (including debt repayment) is the foundation of a retirement plan, having these debts under control in your 40s prepares you for the final stretch.

In Your 50s – Manage Your Risk

The years leading up to retirement and into the first few years of retirement are the most fragile for your investment portfolio. During this time, many retirees have to learn to get comfortable with the fact that there’s no longer a monthly paycheck that hits your bank account. Additionally, this is when financial risk is peaking because the asset base you’ve worked so hard to build now must provide a stream of income that has to last many decades to come.

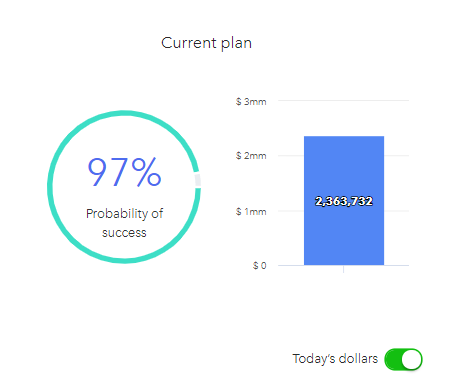

Our hypothetical couple saved diligently throughout their working lives, managed their expenses effectively as a result there is a 97% probability, they successfully retire at 55 and can fully fund their 40-year retirement! And depending on their investment success, they may even have some generational wealth planning to consider as their median wealth to pass on is over $2,000,000 in today’s dollars.

Creating a financial plan during this period to contend with day to day expenses, long-term expenses, and potentially generational gifting can cement your path to a successful retirement. This plan should help you establish not only your financial capacity for risk but also your emotional capacity for risk.

There’s no single path towards a successful early retirement. Some will complete this with abnormally high earnings in their career, while others will pinch every penny to build an extraordinary nest egg. When you get there though, remember, find your reason to wake up each day and enjoy that retirement. Most of us cannot play golf 7 days a week. Stay involved with your community, learn something new, and find out what makes you happy.

Now go enjoy that retirement!

DISCLOSURES

Innova Wealth Partners, LLC (“Innova”) is a registered investment advisor. Information presented herein is for educational purposes only and does not intend to make an offer or solicitation for the sale or purchase of any specific securities, investments, or investment strategies. Investments involve risk and unless otherwise stated, are not guaranteed.

Readers of the information contained on these performance reports, should be aware that any action taken by the viewer/reader based on this information is taken at their own risk. This information does not address individual situations and should not be construed or viewed as any typed of individual or group recommendation. Be sure to first consult with a qualified financial adviser, tax professional, and/or legal counsel before implementing any securities, investments, or investment strategies discussed.

The information on the hypothetical scenario is not based on an actual person or couple and a prospective client should discuss their situation in detail regarding their financial plan. Nothing in the document guarantees success in retiring early.